Medical care pricing can seem puzzling and mysterious to the average patient. Because an insurance plan or other third party is often paying the bill, medical prices are rarely set with the patient in mind. Especially true with hospitals, the arrangements for how providers bill and the prices they are paid are complex and obscured to the point that it is difficult for patients to be prudent consumers of the medical care they receive and at least partially fund. The good news is that patients can ignore many of the most confusing aspects on medical charges and prices, and focus on a few measures to understand the levels charged on medical bills, and gauge what they think is fair.

Billed Charges

The first thing to know about medical bill charges is that they generally have nothing to do with what a provider expects to be paid for services. Hospitals and physicians have scores of different payment arrangements and expectations across sets of their patients. Providers accept or offer different payment rates between government insurance programs (e.g. Medicare and Medicaid), from private insurance plans, for their charity and financial assistance programs, to self-pay/uninsured patients, and across even more categories. A provider’s “standard” charges are billed on all claims to all insurance plans. In many cases, including with Medicare, the insurance plan applies a fixed fee schedule (set dollar amounts) for the services, and the provider’s billed charges are not used to determine the price paid. In other cases, more common with private insurance plans, the insurance plan applies a discount to the provider’s billed charges to determine the price paid.

The incentive is for a provider to set its “standard” billed charges at high levels so they can maximize prices with insurance plans. These high billed charges are not based on what an average patient can reasonably pay on his or her own, but on extraordinary price levels that can take advantage of insurance plan payments to the provider tied on these high charges.

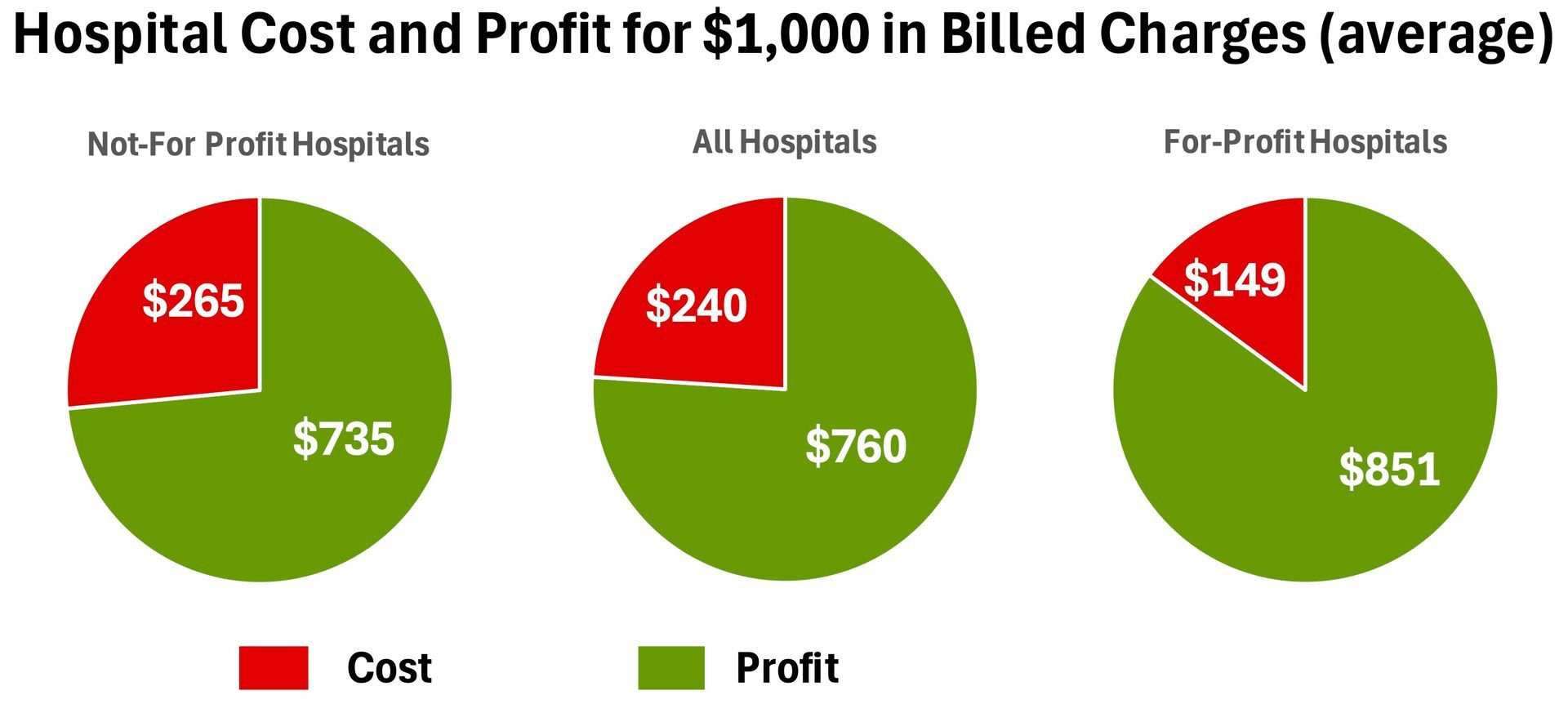

Just how high are these charge levels? Medicare requires hospitals to submit annual reports that track billed charges and costs to provide services. Using these reports submitted by hospitals themselves, the average ratio of hospitals’ costs to the hospitals’ billed charges for the service (“charge-to-cost ratio”) was 417% in 2018. Said differently, on average, hospitals charge over four times more than what it costs to provide services. For every $1,000 billed, $240 covers the cost to render the services and $760 is profit to the hospital. For-profit hospitals average a 671% charge-to-cost ratio. Nonprofit hospitals average 377%.

Beyond hospitals, the level of markup and profit on billed charges varies widely within and between other types of providers. Cost information is not publicly available for physicians and other types of providers beyond hospitals. The important point to remember is that medical billed charges typically have little to do with the cost to render a service, and have the potential, if not the almost certainty, to be grossly inflated compared to cost and what an average patient can afford.

Although providers may adopt unreasonably high charge levels to maximize insurance payments, providers bill those same high charge levels to self-pay and uninsured patients. In those cases in which a provider tries to collect billed charges, the patient needs to be ready to evaluate those charges, and challenge those charge levels when they are unreasonably high and the patient otherwise wasn’t given a Good Faith Estimate of the charges prior to services.

For these reasons, Patient Fairness does not suggest using a provider’s billed charges to determine a fair and reasonable price for a patient to pay.

Insurance Prices

Most health insurance plans have networks of participating providers from which they encourage their members to receive care. Insurance plans negotiate special payment rates with participating provider – Insurance Prices. An Insurance Price is the sum of the insurance plan payment to the provider and the coinsurance, deductible and copayment amounts to be paid by the patient.

The good news about Insurance Prices is that insurance plans usually negotiate discounted prices with a participating network provider below the provider’s billed charges. The bad news is that insurance prices, just like providers’ billed charges, usually have no tie to what an average patient can afford or to the cost to render the service. Many times, an Insurance Price is simply derived using a percentage discount off the provider’s billed charges. An inflated and flawed price (billed charges) is used to set the insurance price, so the insurance price is also flawed. For example, using average hospital billed charge levels, even a 50% discount off charges would yield a 52% profit margin, meaning every $1,000 in insurance prices’ discounted payments contains $520 in profit. What may appear to be a good deal (half off the billed charges) can still be unreasonably high and not affordable to a patient.

Insurance Prices can sometimes even exceed a provider’s billed charges. In those cases, if the patient has a deductible to pay then he or she is paying higher prices than without insurance.

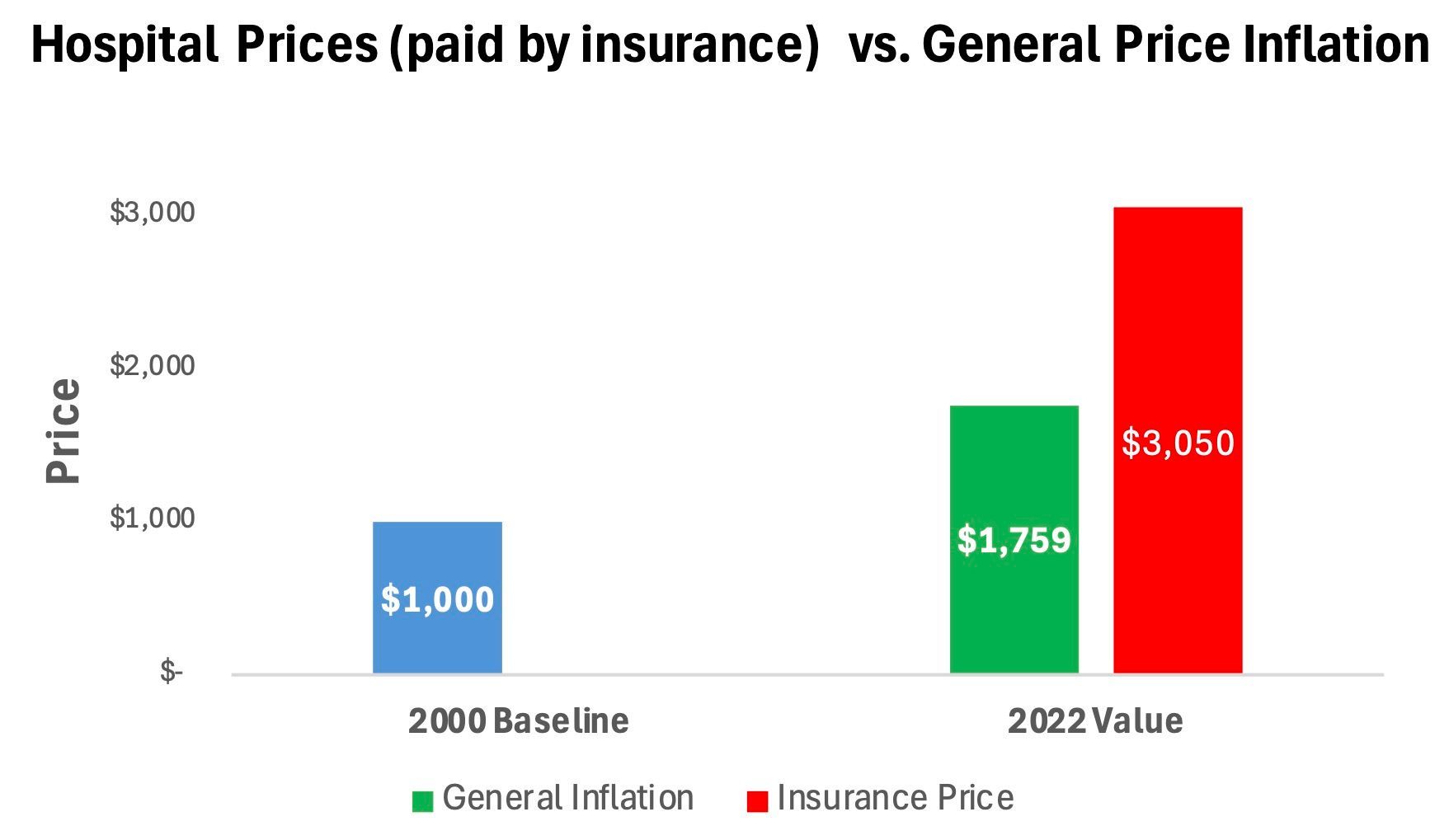

Most importantly, health insurance plans have failed at controlling Insurance Prices. Insurance Prices for hospital services increased nearly twice as rapidly as general inflation since 2000. This means that a hospital service with an Insurance Price of $1,000 in 2000 increased to over $3,000 in 2022, but would have increased to $1,759 under general inflation. Insurance Prices for physician and other services also outpaced general inflation, but to a lesser degree than for hospitals.

For these reasons, Patient Fairness does not suggest using Insurance Prices to determine a fair and reasonable price for a patient to pay. That said, because Insurance Prices are so high, some patients may consider the Insurance Payment Only to yield a sufficient payment amount on its own. An Insurance Payment Only is the insurance plan payment to the provider by itself, without adding coinsurance, deductible and copayment amounts to be paid by the patient. In these situations, the patient may argue that it is fair to settle the medical bill dispute by the provider accepting solely the Insurance Payment Only, and not collect coinsurance, deductible and copayment amounts from the patient. In essence, the Insurance Payment Only is adequate payment to the provider given the issues raised in the dispute.

What to Make of Prices?

If a provider’s billed charges and insurance prices are not reliable levels to help a patient can determine a fair price, what can help?

Patient Fairness uses two comparison measures in its Medical Bill Price Review and tools to help customers evaluate proposals to settle a medical bill dispute – the Medicare fee schedule price and a hospital’s cost to render services. See the article Understanding the Medical Bill Price Review to learn more on how the Medicare fee schedule price and hospital’s cost to render services can help to inform your decision on what is a fair price.